IRS Tax Fraud- What is Tax Fraud?

IRS Tax Fraud: Unraveling the Mystery of What Lies Behind the Numbers.

IRS Tax Fraud- What is Tax Fraud?

Tax evasion is a broad term encompassing the illegal actions taken by individuals, corporations, trusts, and other entities to dodge taxes. This deception involves intentional misrepresentation or concealment of the true financial situation to minimize tax obligations. Such dishonest practices may include, but are not limited to, reporting less income, profit, or gains than were actually earned, or exaggerating deductions.

If you feel you may be at risk, don’t hesitate to contact us today.

What is Tax Fraud?

While the following does not comprise an exhaustive list, these actions may qualify as tax fraud under federal tax law:

- Intentionally underreporting or neglecting to include income that is subject to taxation

- Knowingly exaggerating the value of tax deductions to evade taxes

- Maintaining dual sets of books and records

- Creating fraudulent entries in books and records with the explicit purpose of evading tax obligations

- Misrepresenting personal expenses as business-related

- Filing for fictitious deductions

- Concealing or transferring assets or income to avoid detection

- Failing to report cash income

- Utilizing offshore accounts to obscure income

These examples highlight the various forms that tax fraud can take, all of which are serious offenses under federal law.

Overview of tax fraud and the Internal Revenue Service.

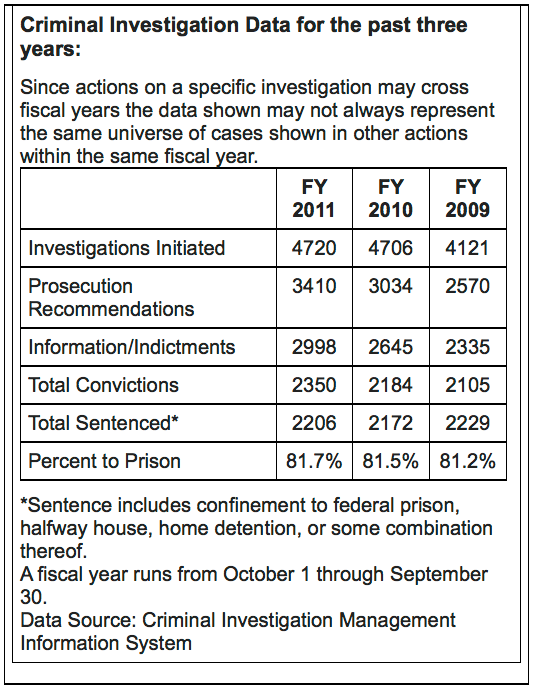

IRS Criminal Investigation consists of around 4,100 staff members globally, roughly 2,700 of whom are Special Agents. Their investigative purview extends to tax laws, money laundering, and Bank Secrecy Act violations.

Although other U.S. federal agencies possess the authority to investigate money laundering and certain bank secrecy act infringements, the IRS is the sole federal body that can probe possible criminal breaches of the Internal Revenue Code.

Adherence to federal tax laws in the United States is largely dependent on a self-assessment of the taxes due. This is referred to as the voluntary compliance system. When individuals or corporations consciously decide to flout these laws, they risk an IRS civil audit or IRS criminal investigation, leading potentially to prosecution and even imprisonment. The IRS often publicizes convictions of tax fraudsters as it encourages voluntary compliance.

Dreis Tax Services, as Criminal Investigators (special agents), occupies a distinct role within the federal law enforcement sphere. With the growing reliance on digital platforms for financial records, these investigators or Special Agents are equipped with the skills to retrieve computer-based evidence, complementing their financial investigative abilities. Special Agents utilize advanced forensic technology to unearth financial data that might be encrypted, password-protected, or concealed through electronic means.

Criminal Investigation’s conviction rate ranks among the highest in federal law enforcement. Convictions not only result in significant prison terms but also entail the payment of fines, civil taxes, and penalties.

IRS TAX FRAUD- WHAT IS TAX FRAUD?

VIOLATIONS, FINES AND PRISON SENTENCES

Title 26 USC § 7201

Attempt to Evade or Defeat Tax:

Any individual who deliberately endeavors to evade or defeat any tax levied by this statute, or the payment of said tax, shall be considered to have committed a felony. Upon conviction, in addition to any other penalties as dictated by law, the individual:

- Shall face imprisonment for a period not exceeding 5 years

- Or be subjected to a fine not exceeding $250,000 for individuals (or $500,000 for corporations)

- Or possibly both, accompanied by the costs of prosecution

These provisions underscore the serious legal consequences of willfully attempting to evade or defeat tax obligations.

Title 26 USC § 7202

Willful Failure to Collect or Pay Over Tax:

Any individual mandated under this title to collect, account for, and pay over any tax imposed, who knowingly fails to collect, or truthfully account for and pay over such tax, shall be considered to have committed a felony. In addition to any other penalties set forth by law, the individual:

- Shall face imprisonment for a period not exceeding 5 years

- Or be subjected to a fine not exceeding $250,000 for individuals (or $500,000 for corporations)

- Or possibly both, accompanied by the costs of prosecution

This provision emphasizes the grave legal repercussions of intentionally failing to fulfill the obligations to collect or pay over the prescribed tax.

Title 26 USC § 7203

Willful Failure to File Return, Supply Information, or Pay Tax:

Any individual obligated under this title to pay any estimated tax, make a return, maintain any records, or provide any information, who intentionally fails to do so at the time required by law, shall be guilty of a misdemeanor. In addition to other penalties provided, upon conviction, the individual:

- Shall face imprisonment for a period not exceeding 1 year

- Or be subjected to a fine not exceeding $100,000 for individuals (or $200,000 for corporations)

- Or possibly both, accompanied by the costs of prosecution

This stipulation highlights the serious legal consequences of deliberately neglecting to file a return, supply required information, or pay the mandated tax.

Title 26 USC § 7212(A)

Fraud and False Statements:

Any person who intentionally makes and subscribes to any return, statement, or other document, containing a written declaration made under the penalties of perjury, and which they do not believe to be true and correct in regard to every material matter, shall be guilty of a felony. Upon conviction, the individual:

- Shall face imprisonment for a period not exceeding 3 years

- Or be subjected to a fine not exceeding $250,000 for individuals (or $500,000 for corporations)

- Or possibly both, accompanied by the costs of prosecution

This provision underlines the serious legal ramifications of willfully engaging in fraud or making false statements on documents associated with tax obligations.

Title 26 USC § 7206(2)- Aid or assistance

Fraud and False Statements:

Any person who intentionally aids or assists in, or procures, counsels, or advises the preparation or presentation of a return, affidavit, claim, or other document that is fraudulent or false in regard to any material matter, regardless of whether such falsity or fraud is with the knowledge or consent of the individual authorized or required to present such return, affidavit, claim, or document, shall be guilty of a felony. Upon conviction, the individual:

- Shall face imprisonment for a period not exceeding 3 years

- Or be subjected to a fine not exceeding $250,000 for individuals (or $500,000 for corporations)

- Or possibly both, accompanied by the costs of prosecution

This clause emphasizes the grave legal consequences of willfully engaging in or assisting with fraud or making false statements in documents related to tax matters.

Title 26 USC § 7206(1)-Declaration under penalties of perjury

Attempts to Interfere with the Administration of Internal Revenue Laws:

Whoever attempts to intimidate or impede any officer or employee of the United States acting in an official capacity under this title, or corruptly or by force obstructs or impedes, or tries to obstruct or impede, the due administration of this title, shall be guilty of an offense. Upon conviction, the individual:

- Shall face imprisonment for a period not exceeding 3 years

- Or be subjected to a fine not exceeding $250,000 for individuals (or $500,000 for corporations)

- Or possibly both

This provision outlines the serious legal repercussions for attempting to interfere with the administration of Internal Revenue laws, including the deliberate intimidation or obstruction of government officials carrying out their duties.

Title 18 USC § 371

Conspiracy to Commit Offense or to Defraud the United States:

If two or more individuals conspire to commit any offense against the United States, or to defraud the United States or any of its agencies in any way or for any purpose, and if one or more of such persons take any action to achieve the objective of the conspiracy, each participant:

- Shall face imprisonment for a period not exceeding 5 years

- Or be subjected to a fine not exceeding $250,000 for individuals (or $500,000 for corporations)

- Or possibly both

This section emphasizes the legal consequences for engaging in a conspiracy to commit an offense against the United States or to defraud it, including collaborative actions that aim to undermine or deceive the government or its agencies.

Contact Us

Thank you for your interest. Please fill out the form to schedule a consultation about your particular tax problem.